What is a mortgage, and should you get one?

Originators or go it alone – the perennial debate in the mortgage space. See my thoughts as expressed in conversation with Isabelle Coetzee in

Read the article online here.

Originators or go it alone – the perennial debate in the mortgage space. See my thoughts as expressed in conversation with Isabelle Coetzee in

Read the article online here.

Last night’s announcement by President Ramaphosa highlights the massive impact COVID -19 is having on all of our lives. Allied to a booze ban and a curfew, we are going to have to deal with many pressing economic decisions and consequences in the coming weeks, not least of these is, should we take a loan from the International Monetary Fund.

My view is that we don’t have a choice and the country is simply out of options. The conditions of such a loan are likely to be onerous and the prospects of default are very real, but we have to take a massive $ 4.2 billion loan (at least) if we are to have any prospect of moving the economy forward and saving jobs and livelihoods.

If Finance Minister Tito Mboweni was an artist, the picture he painted in his Supplementary Budget was not a pretty painting. The portrait of South Africa is terrifying, Edvard Munch’s The Scream is a good comparison. Following the emergency budget, there is going to be much screaming, not least from the trade unions as job cuts are recommended to try and get government spending under control.

However, the true screams of anguish will come when terms and conditions of the large loans the government has so far procured from international banks and financial institutions are revealed, particularly the loan from the International Monetary Fund (IMF). The IMF loan already applied for, of $4.2bn (R72.8bn), will carry stifling conditions. But the whip will be seen when the government almost certainly has to apply for a second longer-term, much larger loan from the IMF. Some conditions will be appreciated by private business and South African citizens, if not by government. Many, though, will be stifling. And they will be around for a long time to come.

Chances are South Africa will have to approach the IMF again for a much larger loan of around $18bn (R298bn), says Ciaran Ryan, an analyst writing for website Moneyweb.

That loan will carry the big stick, for example reforms of SOEs and product and labour markets, he says.

Even with the large loans coming in from abroad, they will probably not be enough to get the economy going again. That could have serious consequences, one being the chance of South Africa defaulting on repayments of its international loans.

“We do not face default yet but when that eventually happens then most international credit lines will not be available anymore,” says Dawie Roodt, chief economist at the Efficient Group. Marius Roodt, senior policy analyst at the Institute of Race Relations (IRR), has a similar view. “There is a serious risk that the government could default on its loans. This would lead to a severe weakening of the currency, as well as the failure of the state to fulfil its duties. It could lead to a severe economic crises in the country unless South Africa gets its debt under control very soon.”

The country already seems to have a severe economic crisis. Yet it could get worse. Mboweni sees this, with the Treasury predicting that revenue will be R1.1trillion instead of the R1.4trillion projected in the main budget in February. Proposed spending is now R40bn more than projected in February. Less income and more expenditure suggests a sure path to bankruptcy, a path many cynics would say the country has already arrived at. This gap between income and spending will mean, Mboweni said, that debt will rise to 14.46% of Gross Domestic Product (GDP), instead of the 6.8% planned for in February. Apart from showing how useless budget predictions are, it also indicates a country not yet bankrupt, but dangerously close to that abyss.

To plug the expenditure gap Mboweni needs additional funding, and that will come from taxpayers’ money. But SA Revenue Services has indicated that due to the sharp slowdown in economic activity, tax collection will be around R285bn lower than expected. What does this mean for the already hard-pressed taxpayer. Higher tax rates?

“The economy contracted by 7.2%. This represents the largest contraction in 90 years,” says banking analyst Simon Stockley. “Of every R1 of tax revenue collected, 21 cents are now being spent on servicing debt.”

All the New Development Bank (NDB) and IMF loans repayments will come from taxpayers, the bulk from individual taxpayers. Is this affordable?

“No. That is why Tito can’t increase this tax much more,” says Dawie Roodt. But even though the tax rates may not be much higher, are individual taxpayers going to be burdened with higher tax rates for a long time to come? “Absolutely”, is Dawie Roodt’s emphatic reply.

Marius Roodt says higher taxes are not fair. “South Africans are already overtaxed. The government should look to cut expenditure by refusing to bail out failing SOEs, cutting the state wage bill, and implementing policies which encourage economic growth, which will lead to higher rates of employment.”

These are conditions that are likely to come with the next IMF loan. We still wait to see exactly what these conditions will be. Sakhile Hadebe, international relations lecturer at the University of KwaZulu-Natal, warns of the still “undisclosed” terms and conditions of international loans. “The country is in a crises, any assistance is welcome although it may be risky. It is an open secret that these international institutions we belong to have an interest in our country. It will be interesting to know the condition of these loans.”

Conditions likely to come with the next IMF loan will probably include cutting the public sector wage bill, up by more than 40% over the past 12 years. “I hope so,” says Dawie Roodt of an IMF imposed cut in public servants pay. “That is the idea.”

“The loan is likely to come with conditions demanding many structural reforms to our economy, such as a cap on wage expansion for government employees and curtailing further borrowing by SOEs,” Stockley says. “We have to accept and embrace those conditions.”

There is another avenue to fund government expenditure to cut debt Mboweni strongly hinted at in his budget. Using pension fund money and assets. “Yes, I think the threat is real. We have seen comments from a number of senior government and ANC officials that pension funds could be tapped,” says Marius Roodt.

If this happens, will it be another case of the government using citizens’ money to pay for their failures? “Yes, the government has squandered the money of taxpayers over the past decade and is now looking to people who have been prudent and saved to fill funding gaps,” says Marius Roodt.

Stockley says governments should just get on and do it. “To fight the notion that we can go it alone is akin to trying to hold back the tide.”

All eyes will now be on the next emergency budget in October to see what government plans next. One intention will almost certainly be to raise an extra R40bn in tax revenue. An inflection point is approaching where taxpayers just can’t afford to pay anymore for government’s IMF loans.

Another grim painting by artist Mboweni? Roll up to get your tickets to the horror art exhibition.

Business & Finance The Natal Witness 28 May 2011.

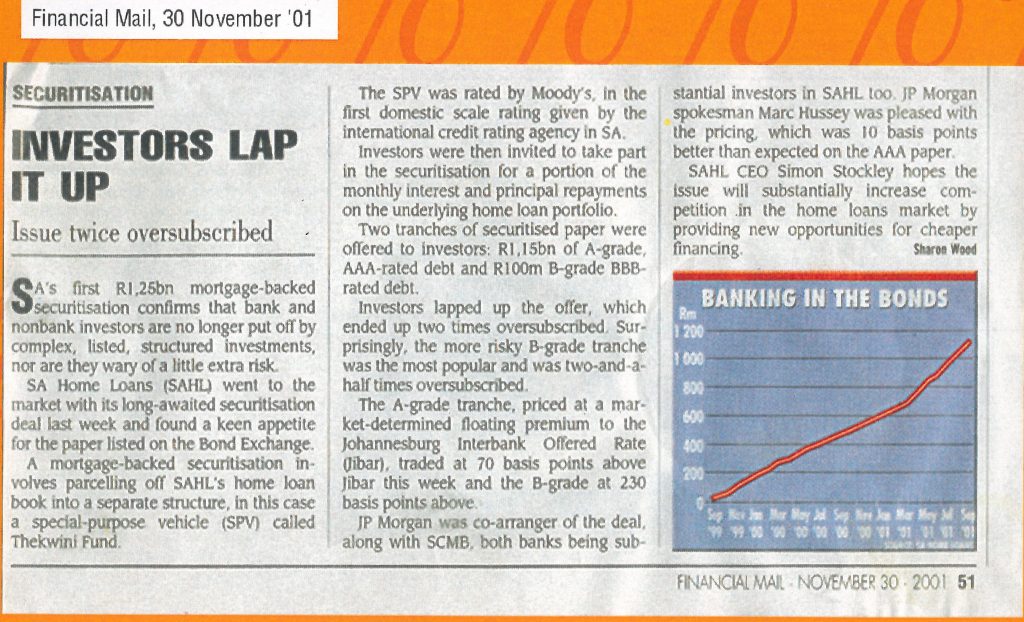

Article in the Financial Mail, published 30 November 2001.