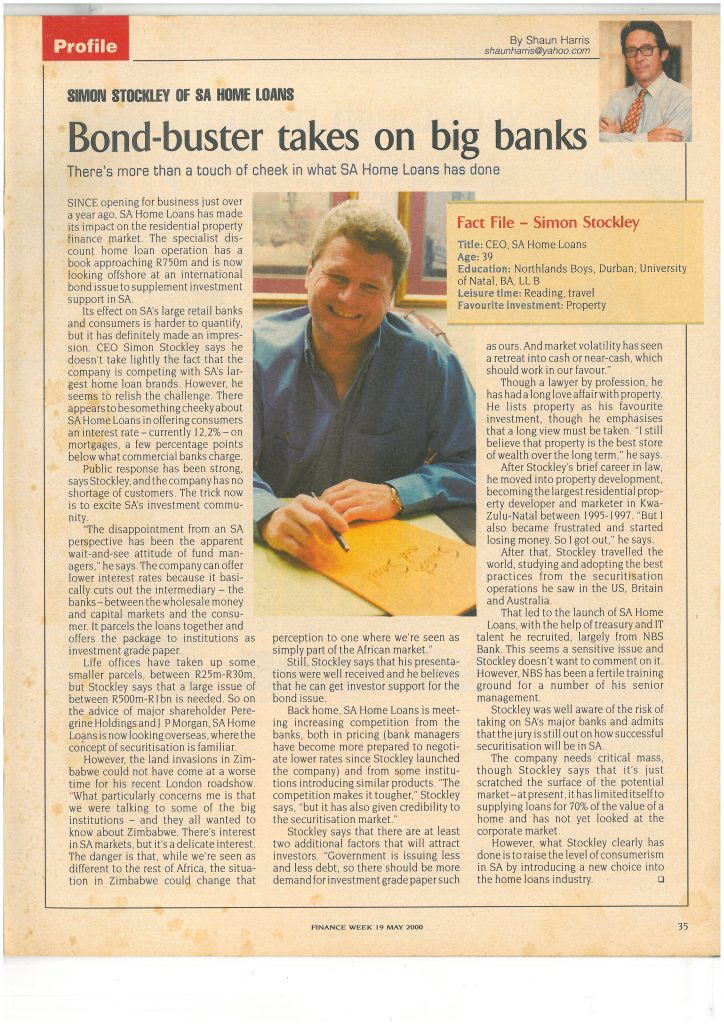

Bond-buster takes on big banks

Published in Finance Week, 19 May 2000

Published in Finance Week, 19 May 2000

The first signs came when Nedbank issued a trading update in late May. Earnings for the half-year to fall by at least 20%, bad debts to rise. This was not unexpected but was still a cold reminder that South African banks, much like banks overseas, are entering a tough period.

Warnings from all the other banks soon followed. All the conditions are against the banks: A flat economy, many clients in financial distress, and interest rate cuts adding up to 275 basis points (bps) so far this year. How bad is it going to get?

“We issued our trading update at our AGM, which happens to be the first of the bank AGM season,” says Mike Brown, CE of Nedbank. “All the other banks have issued similar warnings. It’s a JSE requirement once a company is reasonably certain headline earnings will be more than 20% down on the prior period.”

How bad is it going to get? “The economic fall-out of the Covid-19 lockdown will have a significant impact on the banks’ non-performing loans and credit losses,” says Jonathan Wernick and Alec Abraham, equity analysts at Sasfin Securities. “And the low confidence and negative endowment effect of low interest rates will drag on earnings, not only in 2020 but extending into 2021. While the Bank Index has recovered from its lows in March, it is still some 36% down for the year to date.”

But the situation for banks is not as dire as it could be. Kokkie Kooyman, a portfolio manager and director at Denker Capital, sees opportunities in the gloom. “Based on our research and interactions with management, we believe very few banks will generate losses in in 2020 or 2021 and that they’ll continue to grow shareholder value. In terms of valuations, the financial sector is currently at a larger discount to the MSCI World Index than ever before – indicating it is at the epicentre of fear.

“The fears of seemingly unquantifiable risks have pushed share prices down to levels that create excellent investment opportunities.”

Looking at Nedbank Brown says it’s very difficult to forecast accurately in the current environment. “While we know this year’s earnings will be down on last year, I’m sure that over time bank earnings will recover to pre-Covid levels. What is uncertain is how fast the economy will recover and as a result how fast this recovery in bank earnings will take place.”

Looking at the reasons for banks’ underperformance, banking analyst Simon Stockley, who also heads his own company Catalis, a boutique investment and advisory service, says a combination of factors has created a “perfect storm” for banks.

“Banks are making less revenue from interest charges. Lack of deal flow is likely to affect earnings in the short term and increasing levels of unemployment will make it difficult for average South Africans to service their debt obligations,” Stockley says.

Perhaps the biggest problem for banks is low interest rates, at a low not seen in South Africa for many years. That’s squeezing banks’ net interest income and income margins, which in turn knocks down earnings.

Are more interest rate cuts to come, which will further choke banks’ earnings?

Kooyman says he has no clue what the SA Reserve Bank might do next. “They can’t cut much more. If SARB cuts more they risk further currency weakness. It partly depends on the appetite for emerging markets (EM). If US growth strengthens then capital will flow back to EM for a while. And then the SARB could risk another rate cut.”

Kooyman says globally banks have adapted to lower interest rates by increasingly digitizing and cutting costs. “That is, cutting costs at braches and by less people. In South Africa the unions won’t like that so the process will be slower.”

“Our current forecast is for rates to remain flat from here, with the possibility of one more 25 bps cut this cycle,” says Nedbank’s Brown.

But eventually, earnings growth will start to recover. It might take a long time. How long, for earnings to get back to pre-Covid-19 levels?

“It’s likely to take some time. I would say at least three years. Yet I expect all the banks to bounce back – eventually,” says Stockley.

Kooyman says each country differs according to the depth of the recession, the paid taken and the strength of the recovery. “The US is one of the best cases. We see banks there back to 2019 profit levels by the end of 2022, maybe 2023. In South Africa, I think profit levels will be back by 2023, the latest 2025.”

Brown says in the global financial crises, South African banks’ earnings peaked in 2008 before dropping in 2009. “And three years later, in 2011, they again exceeded the 2008 peak. Much will depend on South Africa’s policy response to the crises.”

With banks under pressure, bank shares have also declined. So what should potential investors do, is now a good time to buy bank shares?

“If you are a potential investor in the sector adopt a wait and see attitude and see how the situation and pandemic develops,” says Stockley. “I suspect prices will still fall before they start to come back. If you are invested in the sector, stay invested. And if you’re thinking of opening a bank anytime soon, don’t.”

Kooyman says bank shares in South Africa are attractively priced. “Like banks all around the world, the quality of lending portfolios is high. Most important to bear in mind in 2020 is that: unlike previous crises, this one doesn’t follow a lending bubble; and banks’ balance sheets have been cleaned up and they hold double the capital they did in 2008.”

Abraham and Wernick from Sasfin Securities don’t believe the current prices of banking shares fully reflect the Covid-19 fallout and the weak medium term South African economic outlook. And as they have said, the Bank Index is still about 36% down over the year.

One point all the commentators agree on is that now is not a good time to start a bank. But while your bank gets poorer, though it will eventually recover, why not get richer buying bank shares.

My recent take on the SARB’s rate cut announcement. Bottom line; it’s a good start but he should have gone a whole lot further and it is now time for other sectors in government top play their part.

The plea from citizens as the bowl of the economy is scraped bare

By Shaun Harris

The recent 50 basis points (bps) interest rate cut by the Reserve Bank was no surprise. Financial markets shrugged it off. Hard-pressed consumers largely welcomed it but also shrugged it off. Which begs the question: should Reserve Bank Governor Lesetja Kganyago have done more? And what should he have done, and what should he do in the future?

“I would have expected 100 bps, but even 50 is useful because lowering debt repayments means there’s a little bit of extra money in the pockets of consumers,” says Economic Justice and Dignity spokesperson Mervyn Abrahams.

Before the Reserve Bank’s announcement of the latest cut banking analyst Simon Stockley was expecting 50 bps but hoping Kganyago might go further. “I do genuinely believe the Governor has latitude to go even further, say 100 bps, but is unlikely to do so, given his historic cautionary approach to monetary policy.”

Now that we know how much lower interest rates are, what do we expect the Governor to do next? “I would be surprised if there was another rate cut so soon after the previous one,” says Magda Wierzycka, CEO and founder of asset management company Sygnia. “Rather I would expect that they will want to ensure liquidity in the market through further bond purchases, as well as stabilizing the banks’ balance sheets. South Africa’s prime interest rate, which is linked to the repo rate, is still relatively high. Consequently there is still further room for rate cuts in the future.”

However interest rate decisions and other means to stimulate South Africa’s crippled economy effectively fall under government. And ultimately, President Cyril Ramaphosa should be, and “should be” must be emphasized, calling the shots.

“The one thing we did not do when the lockdown was declared was to ask questions,” says widely respected political analyst Dr Ralph Mathekga. “The lockdown brought with it a freeze on many important political processes.”

“Excessive use of executive power during the lockdown is dangerous and our politicians must always remember that South Africa is a constitutional democracy and that the lockdown does not mean that the constitution has been suspended even though a few rights were,” says Mathekga.

On Sunday night, May 24, President Ramaphosa announced fewer restrictions when the country moved to Level 3 lockdown. Once again, no surprises, the JSE shrugged off an expected boost to share prices. “The severe interruptions to supply chains, along with a huge loss in incomes, a plunge in the circulation of money and the high levels of unemployment have damaged both supply and demand, while Level 3 still has a number of restrictions to the smooth functioning of the economy,” says Annabel Bishop, chief economist at Investec.

Wierzycka has clear views on the benefits, and restrictions, of Level 3. “It is possible that the relaxation to Level 3 ensures that certain sectors of the economy can spring back relatively quickly. The informal sector is also fairly flexible. However some large employment sectors, such as tourism and aviation, will not recover for a long time.”

“There are no obvious domestic substitutes to absorb the number of unemployed people.”

Stockley is also concerned at the possible spill-out from unemployment. He urges government to recognize how serious the situation is, “with current levels of unemployment, social disobedience and civil unrest is moments away.”

“Government must engage with business constructively. Forget Stalinist centrally controlled solutions to the crises. It is only through forming a social and economic compact with business and citizens that we will emerge from the crises,” says Stockley.

Government’s response to handling the crises through the levels of the lockdown reveals serious splits in the Cabinet and destructive rivalry at the very top.

Government behavior was initially laudable, with the lockdown and mobilizing business support measures, says Sasfin Securities in a report on May 25. But it was “thereafter laughable, with policy confusion and ludicrous measures.” It highlights, says Sasfin, “ongoing factionalism with the ANC and the strength of the corrupt old guard.”

This factionalism has been fed by many rumours. Most serious is of a rift between President Ramaphosa and Minister of Co-operative Governance and Traditional Affairs, Nkosazana Dlamini Zuma. It dates back to before the elections, her role now as possible successor to Ramaphosa should he be indisposed, and the strong support for her with a faction of the ANC.

Rumours, yes, but some rumours have a nasty habit of turning out to be true. It seems Dlamini Zuma’s power extends way beyond her rabid-like fixation on banning smoking.

“It’s time now for all other role players in government to step up to the plate and make a contribution to saving lives and the economy. Inactivity and hesitance is likely to prove more deadly than the pandemic. It’s time to reopen the country, Mr President,” says Stockley.

Wierzycka says “people have run out of money and out of goodwill to comply.” She fears the implications of a possible IMF bail-out. “I don’t have the answers as to what the government should be doing other than to say that it needs to listen to economic and medical advisors rather than making up rules on the fly.”

Bold steps need to be taken. Now.

30 Apr 2020

By Isabelle Coetzee

We all face challenging circumstances at times. For many of us, this may mean we’re unable to afford the basket of goods we usually purchase each month, and for others this may be as drastic as being unable to pay rent.

So, what should you do if you find yourself in the latter category? We got in touch with some industry experts to find out what you can do in these circumstances.

According to Simon Stockley, co-founder and former chief executive of SA Home Loans (SAHL), you should always make an effort to talk to your landlord.

“Negotiation is always better than non-payment. Perhaps agree to a partial rental deferral or a reduction in the rent due, even if only in the short term,” says Stockley.

He recommends being honest and forthright, taking your landlord into your confidence, and negotiating a payment you can afford – but don’t avoid the issue.

“Engaging in dialogue should always be your first option. Landlords are human – they have emotions and (generally) do listen to reason,” says Stockley.

According to Kevin Chetty, director at Xtenda Housing Finance, the best way for a tenant to approach an inability to pay rent is to schedule a phone call with your landlord or the rental agency. He recommends the following:

Are landlords or agencies more lenient?

According to Jan Davel, CEO of PayProp SA, there’s a lot of talk about landlords being more empathetic and flexible towards tenants. However, he points out that if there has been no change in the contractual parties’ rights and obligations, then they’re not obliged to be lenient.

“The Roman-Dutch principle, pacta sunt servanda – which means sanctity of contract or agreements must be kept – is still applicable, even during difficult or unpredictable times. This means that agreements seriously entered into must be honoured – regardless of whether it’s through the landlord or an agent,” says Davel.

However, he adds that it doesn’t mean the contractual terms can’t be renegotiated – it can, and when necessary, it must be renegotiated.

Stockley prefers a direct negotiation between landlord and tenant, without third parties misinterpreting intentions and creating opportunities for conflict. Although, he adds that this can create additional emotional stress in having to deal with a potentially angry landlord.

Sometimes a landlord appoints a managing agent, who has been contracted to collect rental on the landlord’s behalf. Here you will be obliged to negotiate through the appointed agent.

“In all circumstances, but even more so when dealing through an agent, it’s important to keep notes of all discussions and to confirm any changes agreed on or variations to the agreement in writing, so that you can refer to these later if required,” says Stockley.

What if your flatmate defaults rent?

According to Stockley, the obligation to pay the full rental rests with the person named in the lease and the default of a flatmate doesn’t absolve the tenant of the obligation to pay the full rental due to the landlord.

“You have a separate and distinct contractual obligation with your flatmate which, unless it is specifically recorded in the main lease agreement, does not affect it or change depending on the performance of a flatmate,” says Stockley.

He explains that if your flatmate defaults, communication is key. He suggests you immediately notify your landlord and endeavour to negotiate a rent reduction, rental holiday, or a deferral of rental, until the situation normalises.

“Don’t stick your head in the sand; all that it achieves is a restricted airflow and will not magically make missing rent appear,” urges Stockley.

READ MORE: Can banks reject your home loan because of “undesirable” location?

Can you be thrown out if you’re not allowed outside?

During extraordinary circumstances, such as the national lockdown during the Covid-19 outbreak, will your landlord be allowed to throw you out?

“Only in the event that national government publishes a general law amendment act, which suspends or alters the normal operation of the law, will this be prohibited,” says Stockley.

He explains that these can be enacted in situations of grave national crisis, such as drought, war, or pandemic, and are considered so rare and out of the normal they are referred to as “black swan events”.

During the Coronavirus pandemic, South African government appealed to landlords not to go ahead with evictions.

What should landlords do?

According to Grant Smee, founder of EPiC and managing director for Only Realty, a compromise should be reached in the form of a private agreement.

“Each relationship is unique, and this truly is a time for paying it forward. I would encourage landlords with good tenants to come to a compromise if needs be,” says Smee.

He outlines the following tips for landlords who realise their tenants cannot meet their rental obligations:

Cause for Concern ….

The banking sector is likely to be forever altered as a result of the Covid-19 pandemic. I do see the South African banks surviving the crisis, but expect some individual stress and strain.

See my take and that of Mike Brown (CEO Nedbank) below, in conversation with Shaun Harris.

By Shaun Harris

27 April 2020

Banks exemplify solidity. Love them or hate them, people need them for loans, savings and investments. But what now, and what of the future when the coronavirus has eventually passed? What will the banking sector look like then?

Even without the benefit of a crystal ball informed views offer various scenarios of what banks will look like post Covid-19.

“These are unprecedented times for countries, businesses and banks globally – no one can make accurate predictions in this environment, but what we do know is the Covid-19 pandemic and its impact will eventually pass,” says Mike Brown, CEO of Nedbank.

Bank’s financial results and outlooks, however guarded, do give some indication of what banks are going through now in the lockdown and what banks might look like on the other side.

Banks were under pressure some time before the outbreak of the virus, from the ailing South African economy, the rating agencies downgrades, and intense competition between the banks for customers. Then Covid-19 arrived and matters got worse.

It’s reflected in recent results and trading statements from banks. On April 22 Standard Bank released a statement saying “in 1Q20 earnings attributable to ordinary shareholders were 27% lower than in the comparative period.”

A decline of 27% is quite a knock, but the statement goes on to say client credit impairment charges were “significantly higher” in the first three months of the year as businesses struggled with the economic slowdown and nationwide lockdown.”

Nedbank has also taken knocks. Earlier in April more than R5bn was wiped off its market capitalisation in one session on the JSE. Mike Brown puts this in context.

“Our share price on that day reflected the fact that it was the day we traded ex the dividend of R6.95. This is an important aspect many newspapers missed, but investors understand. Our share price has underperformed in 2019, one reason possibly being we are more SA focused than peers and in 2019 the SA economy underperformed versus expectations.”

Simon Stockley, among his various roles a banking analyst, is not too concerned about recent bank results. “I don’t see large scale collapse or consolidation in the sector. Our big five banks are all adequately capitalized, well run and generally have displayed conservative lending criteria, as characterised by the 2008 financial crises which saw, after some initial volatility, all of the major banks surviving the crises and emerging stranger.”

Less upbeat is Ingham Analytics, who view Covid-19 as the “coup de gráce for banks”. They have warned their readers repeatedly about exposure to banking stocks, and say the recent cut in interest rates reinforce their bearish stance.

One bank in serious trouble is the government-owned Land and Agricultural Development Bank, commonly known as the Land Bank. On April 22 it warned creditors that it might default on some R738m of indebtedness scheduled to mature by the end of April due to “a cash crisis it was experiencing.” It also warned of potential defaults on payments on its R50bn bond program.

Yet the Land Bank is a different animal in the banking sector. But still an important animal, providing capital to the farming community. That’s important now. As South Africa starts to ease out of the lockdown farming will become increasingly important. Pre-lockdown stock piling saw many consumers stocking up on frozen and tinned foods. With the retail market returning to normal there will surely be increased demand for fresh produce.

While Stockley does not expect any banks to fail, he does warn that certain specialist lenders will be more adversely affected than the main banks. “Capitec and SA Homeloans are two such cases in point. Capitec because the majority of its lending is in the unsecured sector, where its customers are likely to be under the most financial strain. SAHL because of its unique funding model and reliance on the capital markets for ongoing liquidity.”

Stockley knows SAHL well. He founded the organization and was its first CEO. But while he expects both above examples to suffer stress to their funding models in the short term, “I expect them to both survive.”

But what of the post Covid-19 future for banks? Are plans being put into place now? Nedbank’s Mike Brown responds with an emphatic “Yes”.

“We have a shorter-term focus on resilience and how we operate in lockdown as an essential service. A medium-term focus on how we will transition out of the lockdown, and then a longer-term focus on reimagining how we operate and what we have learnt in this time and as a result what banking may look like in the future.”

Stockley says his prediction is for a more collaborative approach to banking and customer relations. “I see banks adopting a more partnership model to their interactions with customers. Risks and rewards are going to have to be shared more equitably than they have been in the past. In the post Covid-19 reality, they are going to have to nurse their customers back to full health. Those institutions that understand this shift in the balance of power are likely to thrive.”

Back in 1971 the band Traffic produced their greatest album, The Low Spark of High Heeled Boys. In the title track, Steve Winwood sings:

The percentage you’re paying is too high priced

While you’re living beyond all your means

And the man in the suit has just bought a new car

From the profit he made on your dreams

But Winwood goes on:

But today you just read that the man was shot dead

By a gun that didn’t make any noise

And it wasn’t the bullet that laid him to rest

Was the low spark of high-heeled boys

For banks, there is both a warning and encouragement in these words. They have to help clients, sensibly of course, but hard-pressed customers are on the brink of revolt and need help.

Traffic never explained what the “low spark” was in their song. Applied to South Africa, it’s like President Cyril Ramaphosa understood the low spark. He knows starving people who cannot buy bread are on the point of revolution, and is trying, hard, to ease that.

We will all hope he has extinguished the low spark in time.